Installing package into 'C:/Users/Rebecca/AppData/Local/R/win-library/4.3'

(as 'lib' is unspecified)

Warning: package 'Smarket' is not available for this version of R

A version of this package for your version of R might be available elsewhere,

see the ideas at

https://cran.r-project.org/doc/manuals/r-patched/R-admin.html#Installing-packages

Warning: unable to access index for repository http://www.stats.ox.ac.uk/pub/RWin/bin/windows/contrib/4.3:

cannot open URL 'http://www.stats.ox.ac.uk/pub/RWin/bin/windows/contrib/4.3/PACKAGES'

Warning in p_install(package, character.only = TRUE, ...):

Warning in library(package, lib.loc = lib.loc, character.only = TRUE,

logical.return = TRUE, : there is no package called 'Smarket'

Warning in p_load("ISLR", "MASS", "descr", "Smarket", "leaps", "tidyverse", : Failed to install/load:

Smarket

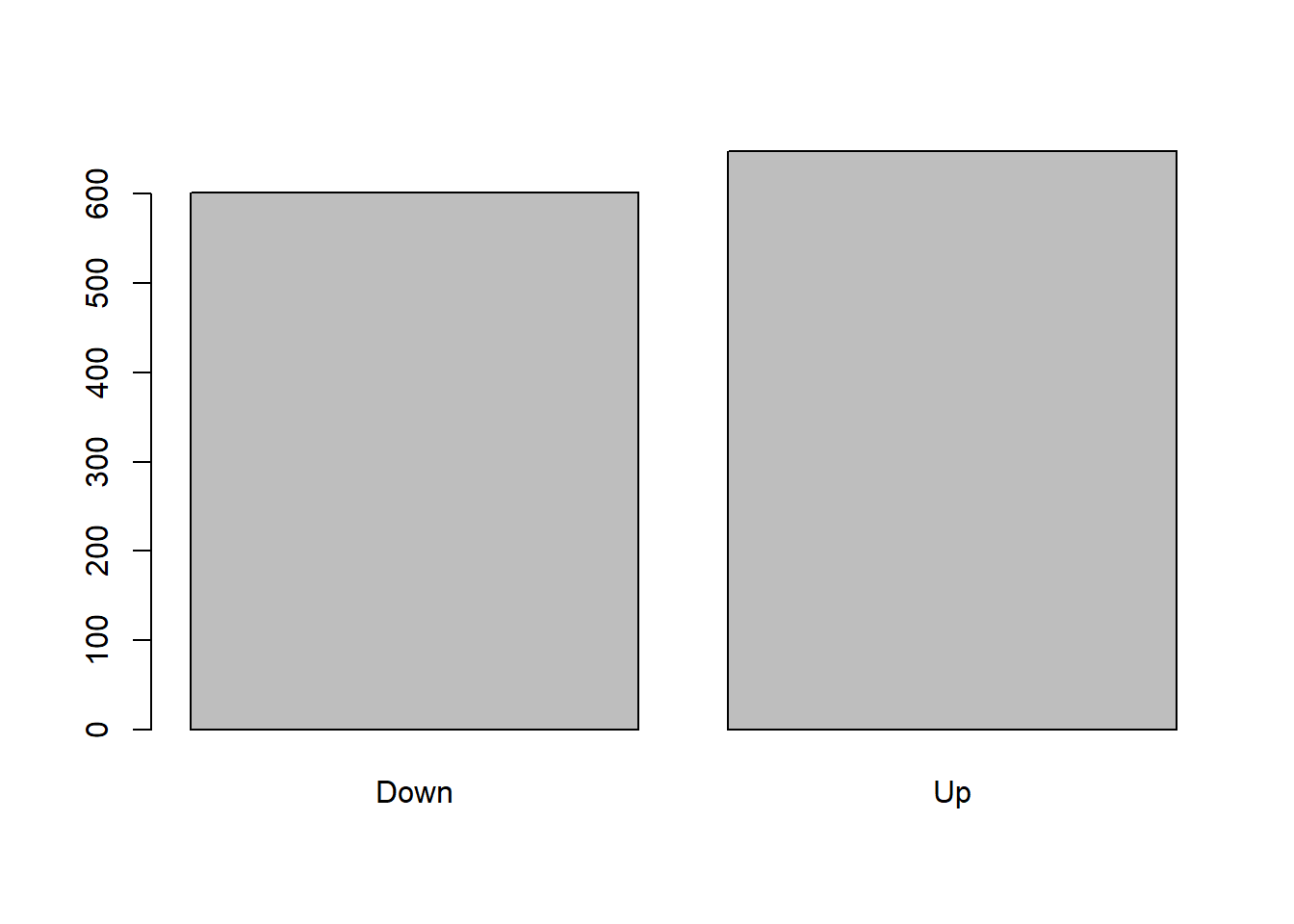

## Make sure libraries are loading. Had some trouble with this. require(ISLR)require(MASS)require(descr)attach(Smarket)## Linear Discriminant Analysisfreq(Direction)

Direction

Frequency Percent

Down 602 48.16

Up 648 51.84

Total 1250 100.00

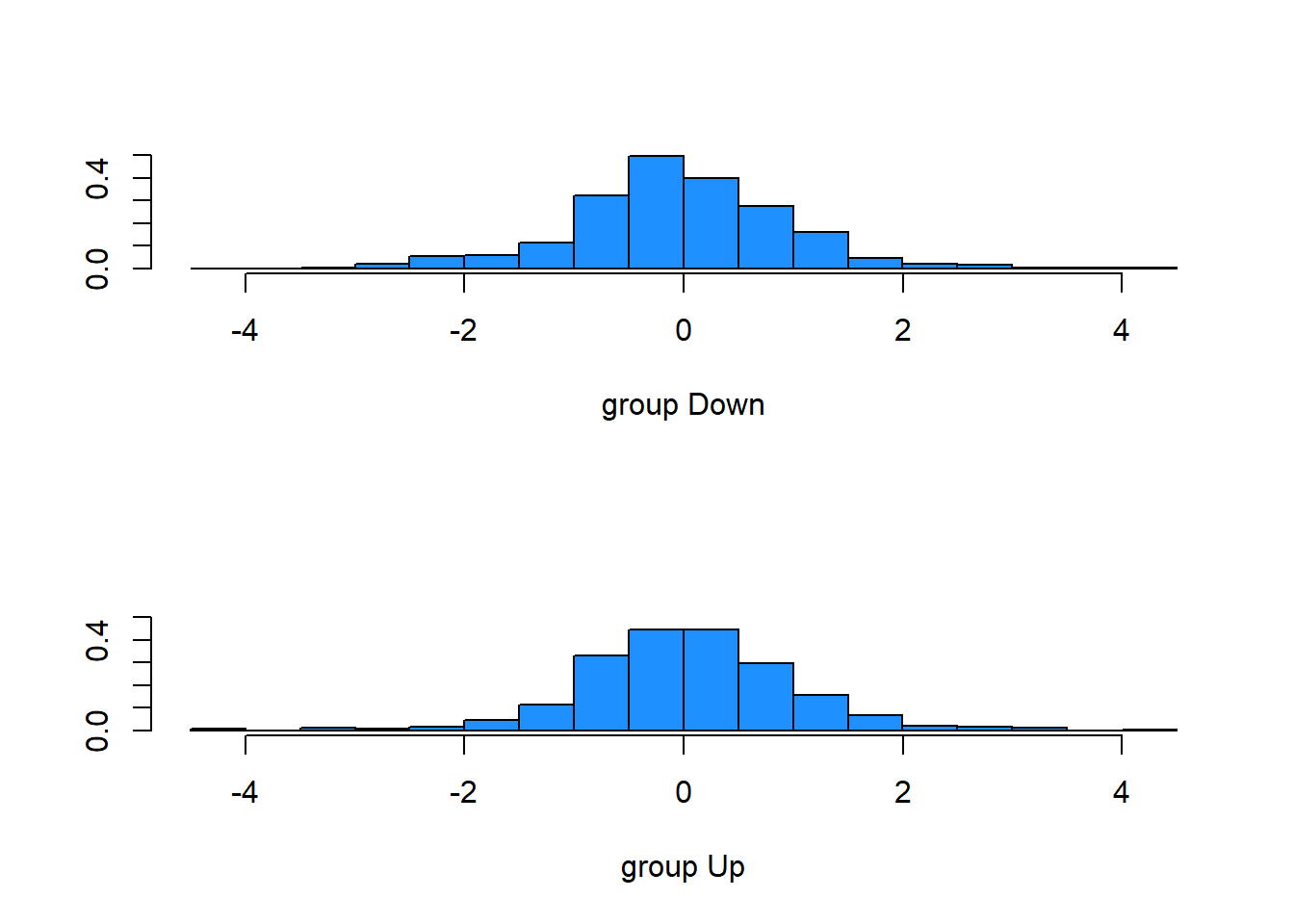

Call:

lda(Direction ~ Lag1 + Lag2, data = Smarket, subset = Year <

2005)

Prior probabilities of groups:

Down Up

0.491984 0.508016

Group means:

Lag1 Lag2

Down 0.04279022 0.03389409

Up -0.03954635 -0.03132544

Coefficients of linear discriminants:

LD1

Lag1 -0.6420190

Lag2 -0.5135293

plot(lda.fit, col="dodgerblue")

Smarket.2005=subset(Smarket,Year==2005) # Creating subset with 2005 data for predictionlda.pred=predict(lda.fit,Smarket.2005)names(lda.pred)

Direction.2005

lda.class Down Up

Down 35 35

Up 76 106

data.frame(lda.pred)[1:5,]

class posterior.Down posterior.Up LD1

999 Up 0.4901792 0.5098208 0.08293096

1000 Up 0.4792185 0.5207815 0.59114102

1001 Up 0.4668185 0.5331815 1.16723063

1002 Up 0.4740011 0.5259989 0.83335022

1003 Up 0.4927877 0.5072123 -0.03792892

table(lda.pred$class,Smarket.2005$Direction)

Down Up

Down 35 35

Up 76 106

mean(lda.pred$class==Smarket.2005$Direction)

[1] 0.5595238

Assignment Questions

From the three methods (best subset, forward stepwise, and backward stepwise):

Which of the three models with k predictors has the smallest training RSS?

Best subset selection has the smallest training RSS. Forward stepwise and backward stepwise have path dependence which can result in an early bad selection impacting the quality of the model overall.

Which of the three models with k predictors has the smallest test RSS?

It depends, because it is possible that all approaches end up with the same model or the forward and backward stepwise select a better model. Generally speaking, again best subset has the smallest test RSS because it considers every model given the input predictors.

Application Exercise

#Generate simulated data set.seed(1)X <-rnorm(100)eps <-rnorm(100)

#Generate a response vector y of length n = 100 according to the modelY <-3+1*X +4*X^2-1*X^3+ eps

#Use the leaps package library(leaps)

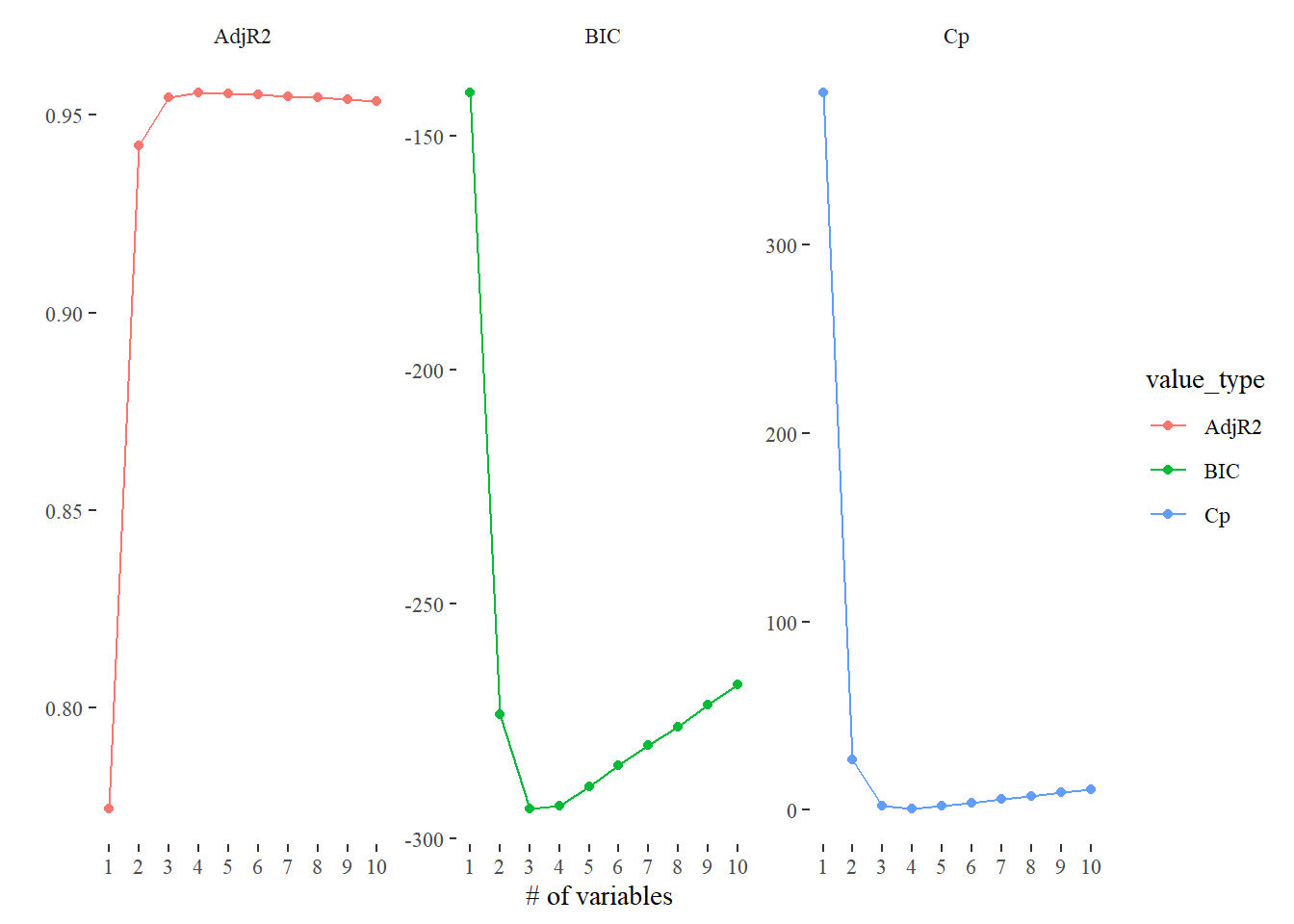

#Use regsubsets() function to perform best subset selectionfit1 <-regsubsets(Y~poly(X,10,raw=T), data=data.frame(Y,X), nvmax=10)summary1 <-summary(fit1)

#What is the best model according to Cp, BIC, and adjust R^2? Show plots and report coefficients. data_frame(Cp = summary1$cp,BIC = summary1$bic,AdjR2 = summary1$adjr2) %>%mutate(id =row_number()) %>%gather(value_type, value, -id) %>%ggplot(aes(id, value, col = value_type)) +geom_line() +geom_point() +ylab('') +xlab('# of variables') +facet_wrap(~ value_type, scales ='free') +theme_tufte() +scale_x_continuous(breaks =1:10)

Warning: `data_frame()` was deprecated in tibble 1.1.0.

ℹ Please use `tibble()` instead.

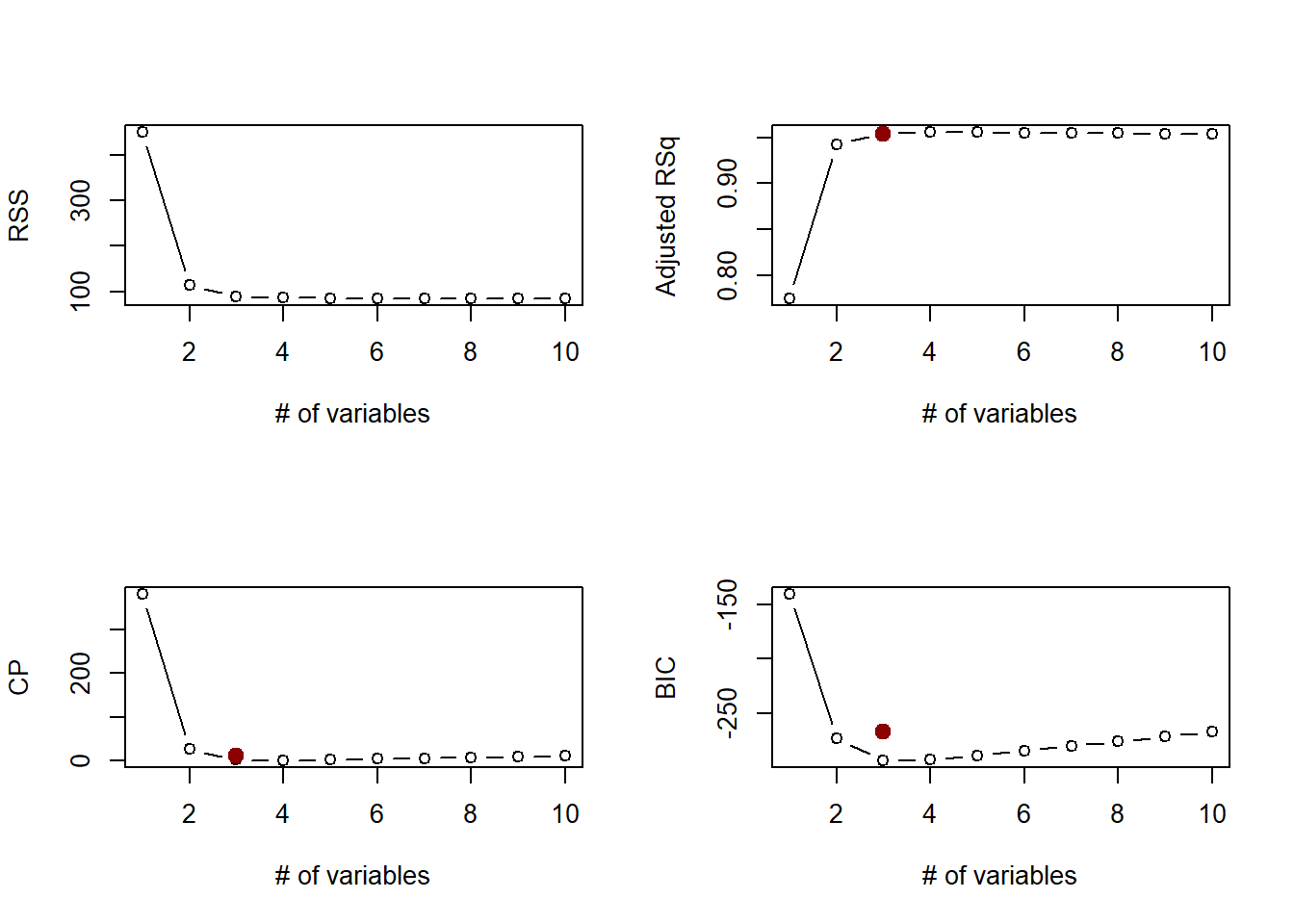

par(mfrow =c(2,2))plot(summary1$rss, xlab ="# of variables", ylab ="RSS", type ="b")which.min(summary1$rss)

[1] 10

points(11, summary1$rss[10], col ="darkred", cex =2, pch =20)plot(summary1$adjr2, xlab ="# of variables",ylab ="Adjusted RSq", type ="b")which.max(summary1$adjr2)

[1] 4

points(3, summary1$adjr2[10], col ="darkred", cex =2, pch =20)plot(summary1$cp, xlab ="# of variables", ylab ="CP", type ="b")which.min(summary1$cp)

[1] 4

points(3, summary1$cp[10], col ="darkred", cex =2, pch =20)plot(summary1$bic, xlab ="# of variables", ylab ="BIC", type ="b")which.min(summary1$bic)

[1] 3

points(3, summary1$bic[10], col ="darkred", cex =2, pch =20)

3 is the optimal number of variables to include as predictors.